Every January, accounting staff & business owners walk into the same old confusing process as they wake up from their holiday slumbers…

*Grabs coffee and begins annual research*

“What is a 1099 again?”

“How do I determine who should receive a 1099?”

“What are the different types of 1099s that need to be reported?”

“Ok… (takes deep breath), what in the world is a 1099-NEC?

WAIT A SECOND, WHEN DID THE PROCESS CHANGE?!!

“I don’t remember ever having to split out 1099-MISC payments from 1099-NEC (sighs).”

*Completes reading new rules*

“I think I get it now, time to print these forms out.”

“THAT’s right, I can’t print them online. Need to swing by Staples to pick some up.”

*Purchases 1099-MISC & 1099-NEC forms*

“I only bought a box of 50 forms, why are there a billion papers in here.”

“Oh yeah… I need to complete 5 form types for each vendor (facepalm).“

“When are all of these due and who do I send them to?”

CAN I GET IN TROUBLE IF I MESS THIS UP??

Fear not! We will break down this process in detail below and explain how PROCAS can help you simplify the reporting requirements. So, keep the Tylenol up in the cupboard, we aren’t going to need it!

The IRS offers a comprehensive breakdown of the changes made to 1099s and all associated forms, deadlines and penalties.

Editor’s Note

This post takes into account the creation of the 1099-NEC (Nonemployee Compensation) form and changes made to the 1099-MISC forms by the IRS for the 2020 fiscal year, covered under the Forms & Deadlines section.

The IRS offers a comprehensive breakdown of the changes made to 1099s and all associated forms, deadlines and penalties.

If you have been using PROCAS to produce your 1099s in the past, we have already done the work in adjusting your system to the new forms and alignment. If not, proceed to learn how the process is completed!

What is a 1099 and why is it important?

1099-NEC & 1099-MISC forms are used to track income of organizations who are not established as corporations (or LLCs taxed as C or S corps). For most companies, 1099 forms will be used to provide an accurate representation of how much non-employees, vendors, sub-contractors, and consultants have been paid throughout the prior year. Because these people and businesses do not receive W-2’s for work performed, 1099s are what the IRS depends on to know how much they owe in taxes for the calendar year.

Who receives a 1099?

Determining who receives a 1099 can be a tricky process. To help, we’ve broken the decision-making tree into the following points:

1) Is the person in question an employee of your organization?

- YES – No need, they should have received a W-2.

- NO – Independent contractors and consultants will most likely need a 1099, proceed to Question 3.

- NOT SURE – Consider the following questions:

- Do you provide benefits to this individual?

- Do you provide equipment, office space, or materials for the individual to complete their job?

- Do you reimburse business expenses incurred by the individual?

- Are you the sole client or primary client of the individual? And do you completely control their weekly workflow?

- NOT SURE – If you answered NO to all the above sub-questions, proceed to Question 3.

- NOT SURE – If you answered YES to any of the above sub-questions, you may be considered that individual’s employer in a court of law and may need to start providing W-2 information. Consider seeking a labor lawyer’s advice.

2) Is the vendor you purchased services from a corporation?

- YES – No need to send a 1099.

- NO – Sole Proprietorships and Partnerships will most likely need a 1099, proceed to Question 3.

- NOT SURE – LLC’s are the most confusing of the bunch. To determine how the company is taxed, please send a W-9 to that vendor’s accounting staff. Once returned,

- If taxed as S Corp or C Corp, no need to send 1099.

- If taxed as sole proprietorship or partnership, proceed to Question 3.

3) How much money was paid to individual or vendor?

- Anything less than $600 total for the calendar year does not require a 1099.

- Any payments totaling $600 or more will require a 1099.

- Common Exceptions:

- $10 or more in royalties will require a 1099

- In general, payments made to law firms will require a 1099

- If paid via credit card, a 1099 is not required (even in excess of $600). The credit card company will take care of the reporting for you.

- Business expense reimbursements for employees will not require a 1099.

Forms & Deadlines

For fiscal year 2020, the IRS has separated out nonemployee compensation from other standard types of miscellaneous payments into two forms – 1099-NEC & 1099-MISC.

1099-NEC forms now require the following payments be submitted:

- Cash payments made to nonemployees

- Prizes and awards for services performed by nonemployees

- Cash payments for fish

- Payments by a federal executive agency for services

- Gross oil and gas payments for a working interest

- Taxable fringe benefits for nonemployees

All other types of payments will still be listed on the 1099-MISC forms. Alignment of the remaining boxes on this form has shifted, which we have already adjusted for you in PROCAS! Please see Utilizing PROCAS to complete your 1099s for how we’ve modified to the new forms.

1099 Forms

Each set of forms contain 6 parts to be filled out and sent to their appropriate recipient(s):

- Copy A – For Internal Revenue Service Center

- Copy 1 – For State Tax Department

- Copy B – For Recipient

- Copy 2 – To be Filed with Recipient’s State Income Tax Return, When Required

- Copy C – For Payer

- 1096 – Completed with each set of 1099s

Deadlines

While these forms can be generated around the same time, they typically are sent separately at different deadlines:

- January 31st

- File 1099-NEC Copy A forms and 1096 with the IRS

- DO NOT mix in 1099-MISC Copy A forms

- Can also e-file if preferred

- Send 1099-NEC Copy B forms to recipients

- File 1099-NEC Copy A forms and 1096 with the IRS

- February 28th

- File 1099-MISC Copy A forms and 1096 with the IRS

- Send 1099-MISC Copy B forms to recipients

- March 31st

- Deadline to e-file to the IRS for 1099-MISC Copy A forms and 1096

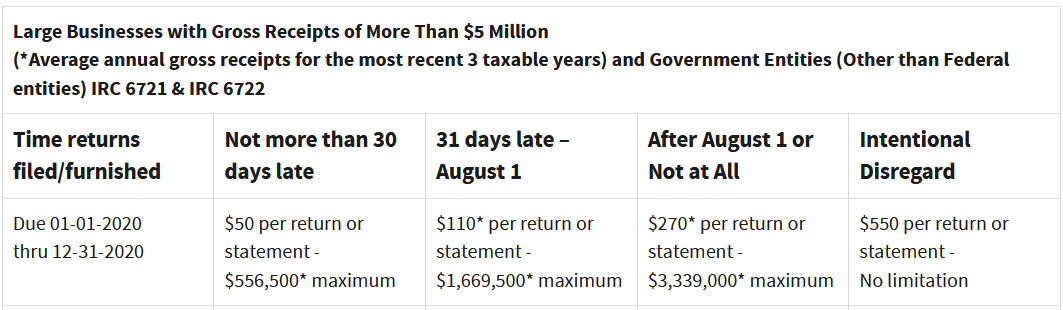

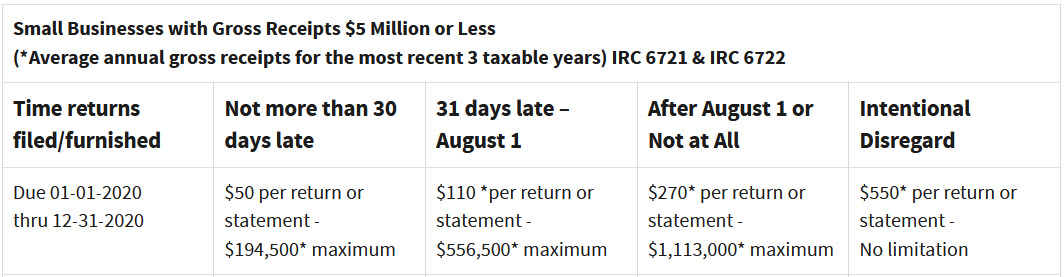

PENALTIES

Failure to submit accurate 1099 forms by the required deadlines can be costly for businesses. The below charts are taken from the IRS’s publication on potential penalties and fines for failure to submit 1099s.

Large Businesses with Gross Receipts of More Than $5 Million

Small Businesses with Gross Receipts $5 Million or Less

As you can see from the above charts, proper submission of 1099 forms to the IRS is one that should not be taken lightly.

Utilizing PROCAS to complete your 1099s & 1096s

PROCAS currently supports four types of 1099s: 1099-NEC (nonemployee compensation), 1099-MISC (all other payments), 1099-INT, and 1099-DIV, as well as 1096s. Each form can be generated out of the system by following these 3 steps:

- Determining which vendors/subcontractors require 1099s

- Establishing 1099 form type and box by vendor/subcontractor

- Generating 1099/1096 forms from PROCAS

1) Determining which vendors/subcontractors require 1099s

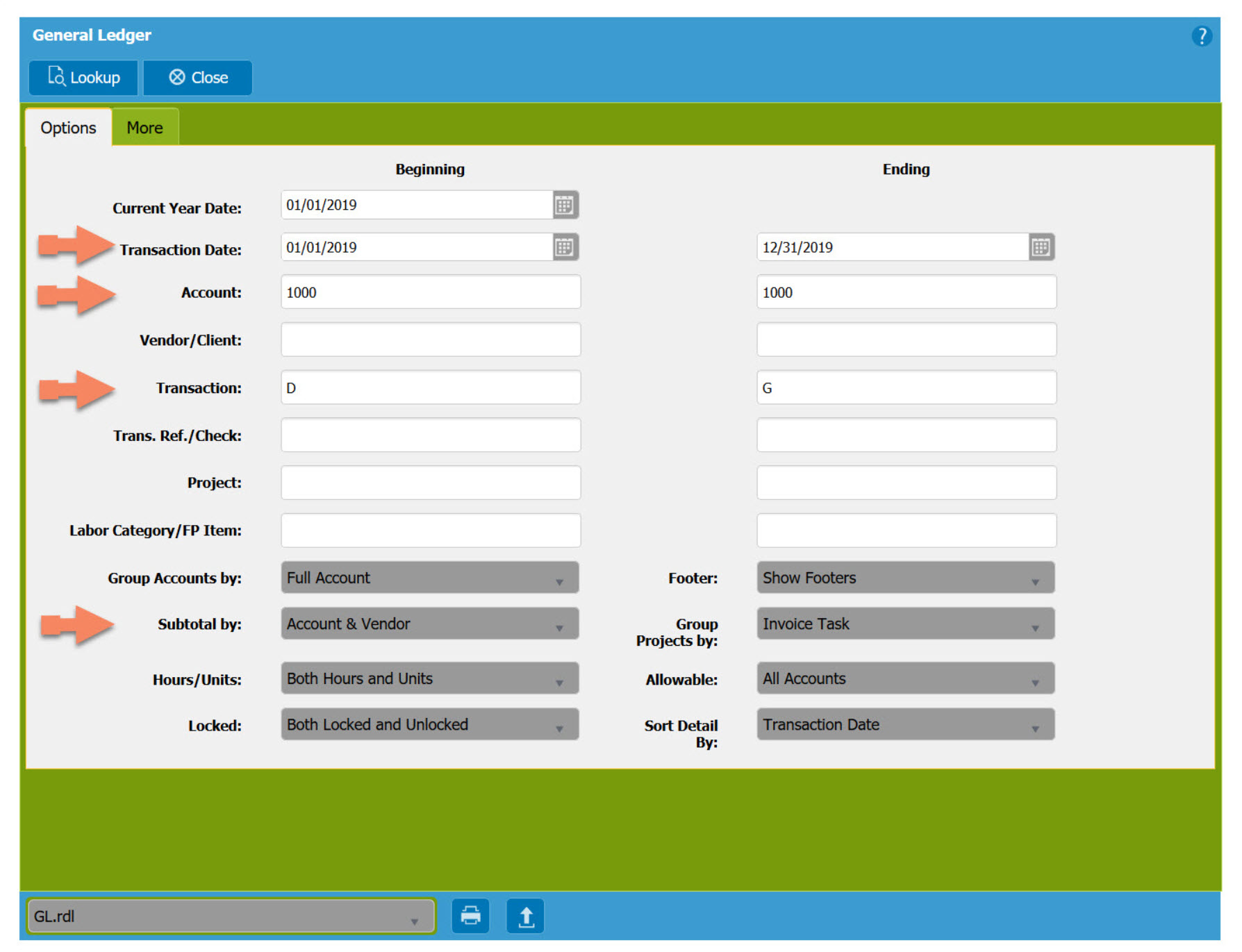

In order to find out who you paid money to in the prior year, please go to the following:

Accounting –> General Ledger –> General Ledger

Here, use the parameters next to the orange arrows below to generate a report for cash payments made in the following year.

- If you conduct electronic batch payments (ACH or EFT), open up the account range to include AP accounts along with cash.

Once you’ve printed your report, please follow the above section “Who receives a 1099” to whittle down your list of possible vendors to those who should receive a form.

2) Establishing 1099 Form Type & Box by Vendor or Subcontractor

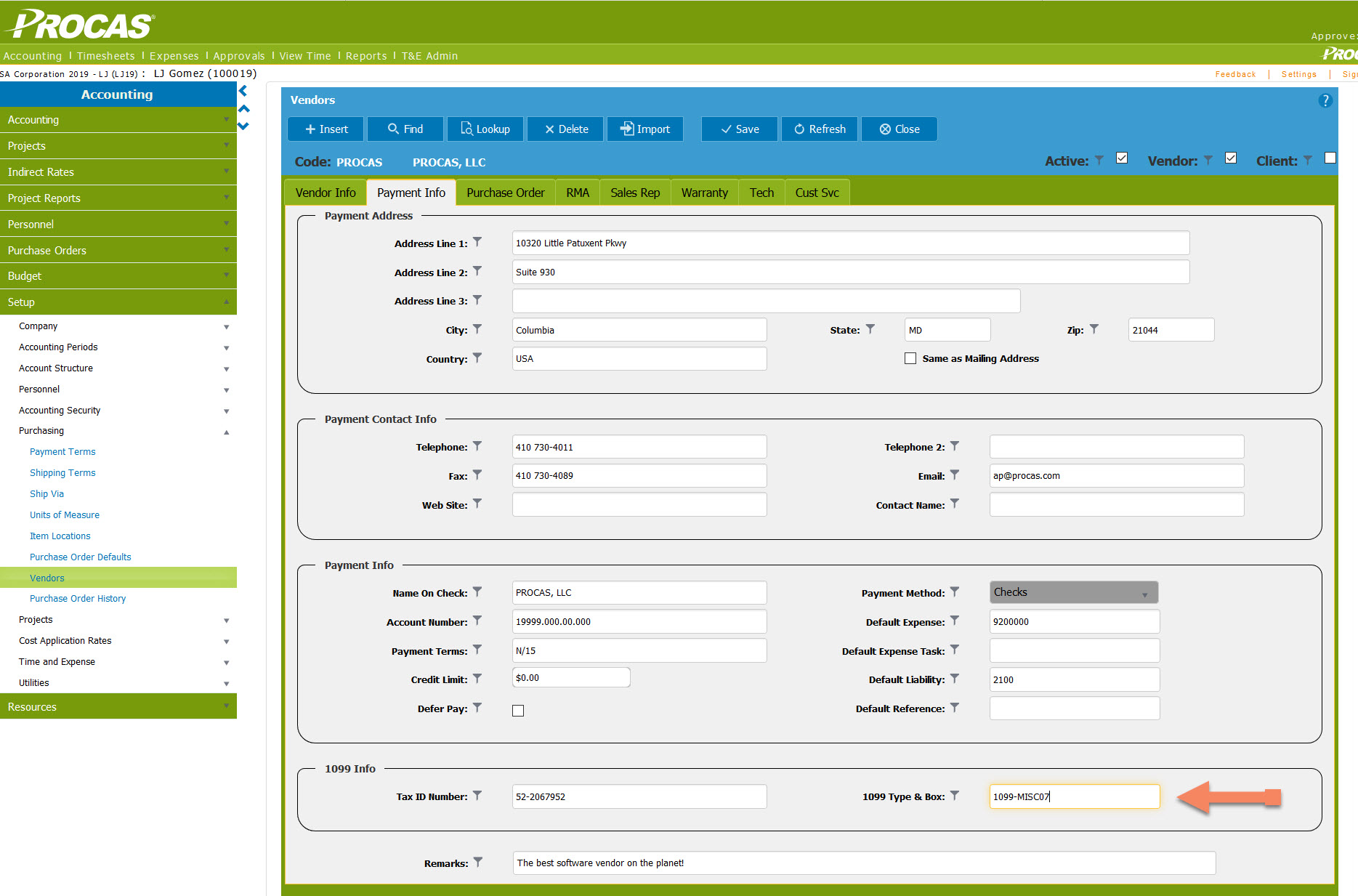

Now that you have your list of vendors and subcontractors, time to label their records as to which type of form they should receive. Please navigate to:

Setup –> Purchasing –> Vendors

And select the “Find” button or “F8” function key to begin searching for those vendors/subs. Once on the record of an applicable vendor/sub, select the “Payment Info” tab of the record to locate a box called “1099 Type & Box.”

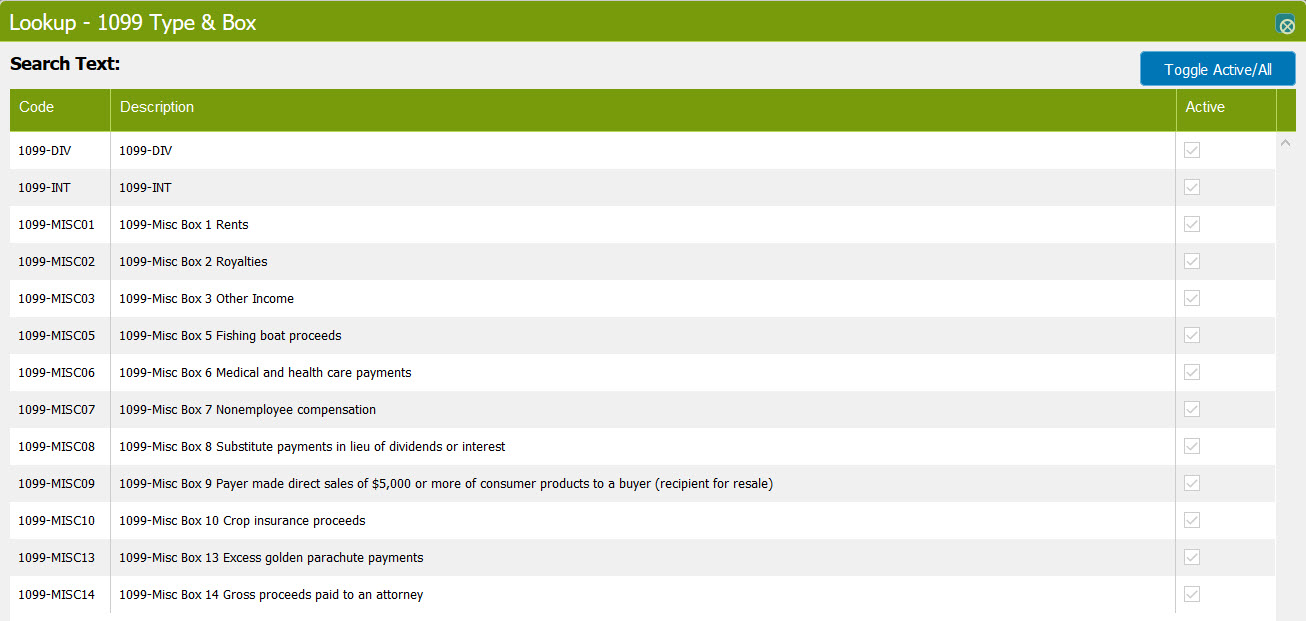

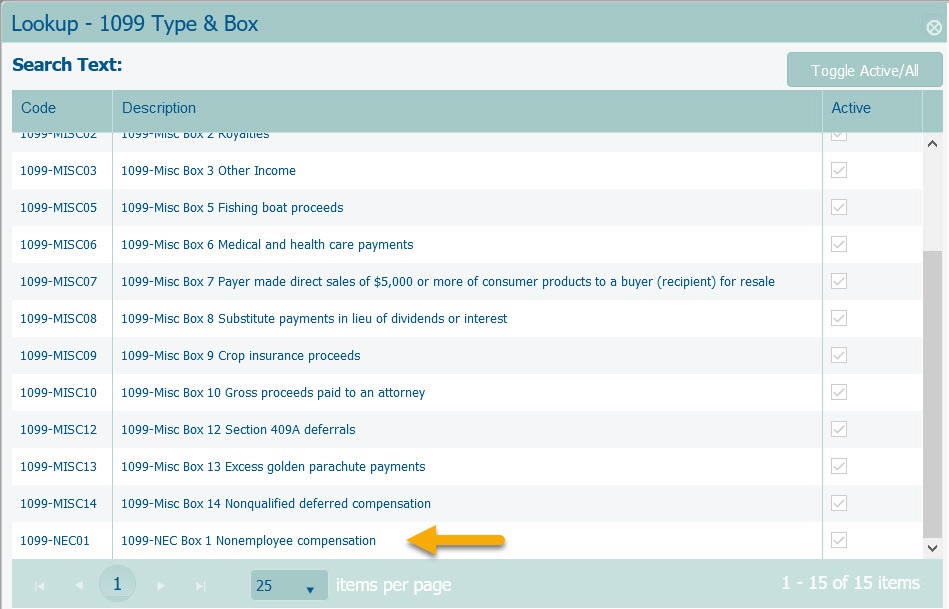

If you click in this box, you can then select the “Lookup” button or “F9” function key to see the list of possible 1099 types.

From the above list, make the appropriate selection for each vendor/subcontractor as needed.

Editor’s Note – 2021

If you have established this list in prior years, we have remapped your vendors to the new form & box types. 1099-MISC07 has been modified to 1099-NEC01 for Nonemployee Compensation and remaining 1099-MISC boxes have been modified for the new form alignment. You do not have to complete any extra work in remapping existing vendors!!

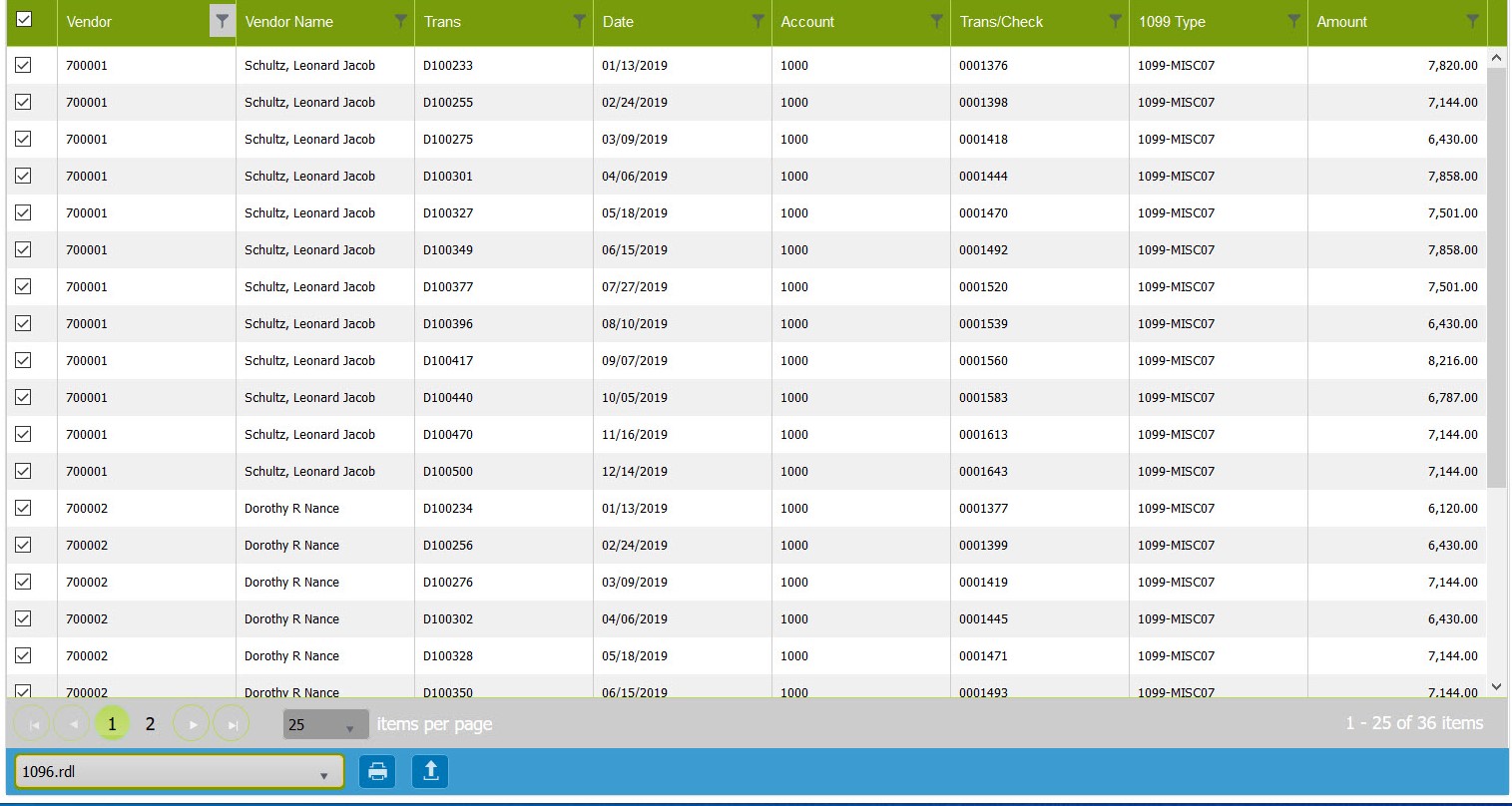

3) Generating 1099 & 1096 forms from PROCAS

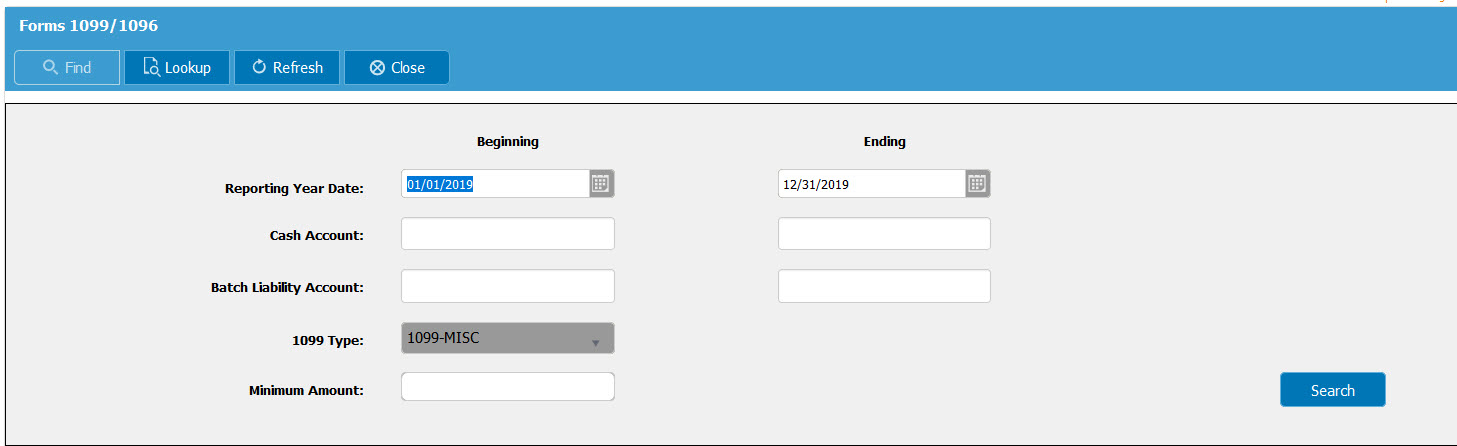

Once all 1099 types and boxes have been determined, navigate to the final menu:

Accounting –> Accounts Payable –> Forms 1099/1096

This screen will be broken into two separate parts to get the appropriate items needed to print your forms:

The header section of Forms 1099/1096 has specific parameters to determine which items will generate in the detail grid:

- Reporting Year Date – Use the prior calendar year for as is required for reporting 1099/1096 amounts.

- Cash Account – Use the cash account recorded in the GL for payments made to each vendor/sub (if left blank, all accounts will generate).

- Batch Liability Account – If you make payments in batch from your bank account, enter the liability account used here. Leaving this area blank will populate all possible payments.

- 1099 Type – Choose applicable 1099-NEC, 1099-MISC, 1099-DIV, or 1099-INT.

- Minimum Amount – This will limit the results by taking the sum of all payments by vendor, and exclude them if the total is less than the minimum entered.

- Search – Will populate below details.

In this detailed grid, select the payments made to each vendor if you are looking to include them on your forms. When all appropriate rows have been selected, print the proper 1099 or 1096 report from the below report bar.

- Each column has the ability to sort items if you click the column header

- Each column also has the ability to filter items if you select the filter icon to the right of each column header

Extra Help & Form Alignment

For additional help completing your 1099/1096 forms using PROCAS:

- In the upper right hand corner there is a “?” symbol, which will provide in-system help for detailed instructions on any of the menus!

- Feel free to reach out to our Support Team at support@procas.com

- We can help align your report forms to your printer specs as well as help explain the process.